16/09/2024

Results at a glance:

- Australian rural confidence has improved this quarter, fuelled by positive market signals and useful winter rain in a number of regions.

- Confidence improved in all states, with Tasmania recording the biggest U-turn, and in all commodities except for cotton.

- Investment intentions remains stable.

Confidence has returned to Australia’s farming sector following a mid-year dip in sentiment, as more favourable livestock markets and beneficial rain in some cropping areas fuel renewed optimism.

The quarter three Rabobank Rural Confidence Survey, released today, found sentiment among the country’s agricultural producers had rallied heading into spring, although farm sector confidence remained just shy of net ‘positive’ levels – with still slightly more farmers holding a pessimistic outlook than those expecting a better year ahead.

Farmers had begun the year with a surge in optimism, but sentiment had fallen by mid-year due to the worryingly late – and in some cases no – ‘autumn break’ for winter cropping regions, especially in Western Australia and South Australia.

However, beneficial rainfall in the west and along the eastern seaboard put the brakes on sliding seasonal confidence this quarter. And improved prices for sheep and beef producers also supported optimism about the agricultural economy ahead.

Farmer confidence improved in every state, although only New South Wales and Tasmania recorded net positive sentiment (with more farmers expecting conditions to improve than deteriorate). Confidence also lifted in all commodity sector surveyed, except for cotton.

Rabobank group executive for Country Banking Australia, Marcel van Doremaele said more promising market signals, particularly in the livestock sectors, along with positive seasonal conditions and production outlooks in many parts of the country, had resulted in farmers taking an overall more bullish view this quarter.

“Although some parts of the country are still grappling with the impacts of unusually dry weather through autumn and winter, it’s encouraging to see the patchy start to this year’s season have been corrected in many farming regions, especially in WA where seasonal conditions looked dire last quarter but have really turned around,” he said.

“Farmers are still managing challenging conditions in south-west Victoria and across South Australia which continue to put pressure on winter crops and feed for livestock. And grain growers in these regions are particularly holding hope for good spring rainfall to finish crops following the very dry winter.

“The ENSO (El Niño Southern Oscillation) Outlook remains at La Niña watch – meaning there are signs La Niña may develop later in the year and the potential for a wetter spring has held promise during the survey period, which has helped confidence track back up.”

Mr van Doremaele said shifts in key commodity markets had also helped to boost farmer confidence this quarter. “Livestock producers are more optimistic after improvements in cattle and sheep prices, and there are also positive signals for dairy production. Grain and cotton farmers though face more bearish conditions with global drivers putting downward pressure on prices,” he said.

“There are also encouraging economic drivers underpinning farmer sentiment, including interest rates, with market forecasts of cuts in the official cash rate next year. In addition, the high cost of farming inputs, such as fertiliser, has also been easing, which is especially critical to farmers’ ‘bottom lines’, taking into account the impact of depressed grain markets.

“So, some easing of economic pressures, combined with useful winter rainfall for those regions which received it, has seen many farmers are tracking towards the end of the year with a more positive mindset. Others though do remain glued to the outlook and in need of a wet spring to finish crops and replenish feed reserves to ease pressure on feeding livestock.”

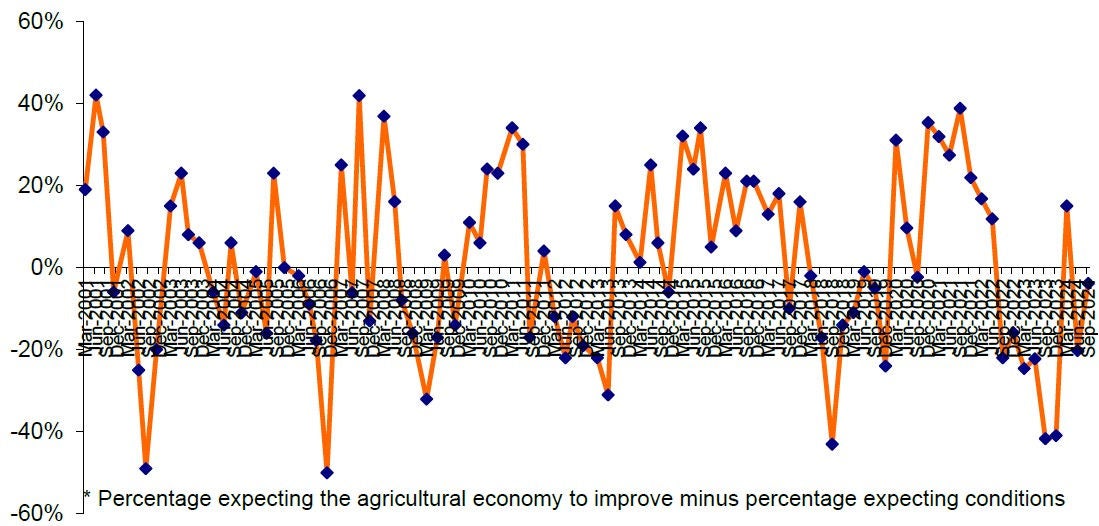

The Q3 survey, completed last month, found those Australian farmers expecting the agricultural economy to improve in the coming 12 months had increased to 23 per cent (from 15 per cent with that view in the previous quarter). And fewer respondents (27 per cent) were now expecting conditions to worsen (down from 36 per cent).

A similar number to last quarter (47 per cent) had a stable outlook on the year ahead, anticipating the agricultural economy to remain the same.

Key drivers for optimism in the sector were found to be a positive outlook on commodity prices (nominated by 32 per cent) and good seasonal conditions (31 per cent).

While drought remained the leading worry for farmers – nominated by 31 per cent – this was down on 37 per cent with that concern last quarter. There was also less concern about rising input costs (cited by 29 per cent, down from 35 per cent) and falling commodity prices (22 per cent, dropped from 32 per cent).

Interest rate worries remained stable quarter-on-quarter, although there was increasing concern about the threat to live export, following the announcement in July that live export of sheep will end in May 2028.

States

While there was an upturn in farmer confidence across all states, sentiment levels varied considerably.

Tasmanian farmers are the most optimistic in the country, with net confidence levels jumping to 40 per cent, up from -16 per cent just three months ago. Improved cattle and sheep markets supported the improved outlook, while prolonged dry conditions were broken by some useful winter falls of rain, although many parts of the state have more recently grappled with an overabundance of rain in recent weeks.

New South Wales was the only other state to climb back into net positive confidence levels, lifting to one per cent from -11 per cent in the previous quarter. The move back into positive territory is founded on easing concerns about drought and commodity prices in the state.

While many Victorian farmers are still managing unusually dry seasonal conditions in parts of the state, a reasonable season in northern regions helped to drive a lift in farmer confidence. A quarter of Victorian farmers are now hopeful conditions will improve, pushing net confidence levels from -31 per cent to -4 per cent this quarter.

Queensland’s rural confidence climbed thanks to solid seasonal conditions and rising commodity prices. Net confidence now sits at -4 per cent, up from -13 per cent, supported by expectations of typical seasonal rainfall conditions in coming months.

South Australia’s rural sector reported the lowest sentiment in the country – subdued by below-average winter seasonal conditions – but net confidence still lifted from -38 per cent to now sit at -27 per cent. Confidence in red meat markets provides a much-needed shining light in a state where livestock producers are reassessing feed budgets and grain growers are recalibrating their yield expectations as they roll towards harvest.

Farmer confidence lifted in Western Australia, to -8 per cent from a net -21 per cent last quarter. Increased concerns about the threat to live export – now that a deadline has been formally announced for the end of the live sheep trade – were offset by seasonal relief from much-needed rainfall which fell across the state’s wheatbelt during winter and improved domestic sheep and cattle markets.

Commodities

While cotton had been the only commodity to report a lift in confidence in the previous (quarter two) survey, the tables turned this quarter, with cotton the only sector to report a decline in sentiment. The key reasons for dwindling optimism among cotton growers were falling commodity prices and concerns about overseas markets/economies – reflecting forecasts of an increase in global cotton supply in the 2024/25 season, alongside demand-side headwinds, which is weighing on prices for Australian producers.

Confidence among the nation’s grain growers climbed, but remained at net negative levels, at -19 per cent. Grain growers had relief from improved seasonal conditions and some easing in input prices and were also optimistic of a turnaround in prices – despite the current bearish conditions for wheat and barley and softer prices for canola.

“Favourable seasonal conditions in New South Wales and Queensland, supported by a better-than-anticipated winter growing season in Western Australia, is driving crop production with ABARES currently forecasting national winter production to increase to 55.2 million tonnes in 2024-25 – which is 17 per cent above the 10-year average,” Mr van Doremaele said.

“However, growers in South Australia and western and northern Victoria have recalibrated their crop expectations after unfavourable growing conditions – many are simply hoping to get their seed back.

“And with domestic wheat prices pressured by a combination of the downward trend in global prices combined with promising yield prospects in other Australian grain-growing states, this will have implications for margins for growers.”

Beef producers were encouraged by solid cattle prices, with improvements through July for cows and heavy steers. Young cattle prices are also starting to move up as the impact from global beef demand – especially from the US – flows back to the Australian market to help elevate prices. This pushed net confidence for the beef sector into positive territory this quarter (10 per cent, up from -6 per cent).

“Rabobank analysis points to cattle prices continuing to track upwards in coming months,” Mr van Doremaele said.

Sheep producer confidence took a leap forward this quarter, riding on the back of an improved seasonal outlook and commodity prices.

“Net sentiment tipped back into positive territory (one per cent, was -37 per cent) for the sheep industry, with more favourable seasonal conditions in many regions and the prospect of stronger prices giving them hope for the coming year,” Mr van Doremaele said. “However, sheep producers remain very concerned about government policies – especially the threat to live export – with WA’s sheep industry in particular bearing the brunt on the long-awaited, finally received hard deadline for live exporting sheep, which was handed down prior to this survey.”

Confidence also improved among the country’s dairy producers, in line with the continuing recovery of Australia’s milk production and only modest global supply growth forecast for the year ahead.

“New South Wales leads the charge with milk production, supported by favourable seasonal conditions, whereas severe rainfall deficiencies for milk producing regions in western Victoria and South Australia have impacted supply in these areas. However, the outlook among dairy farmers is brighter, driven by expectations of improved seasons and domestic market conditions.”

Most of the nation’s sugar cane growers anticipate that agribusiness conditions will remain stable over the year.

Investment and incomes

The nation’s farmers also reported a slight increase in appetite to invest in their farm businesses this quarter. More planned on increasing their level of investment in the year ahead (24 per cent, up from 21 per cent last quarter) although 14 per cent intended to invest less (compared with 13 per cent previously).

More farmers also expect their farm incomes to increase over the next 12 months – 30 per cent (up from 21 per cent last quarter), while the number expecting a lower income had declined to 27 per cent (from 32 per cent).

“Despite seasonal variability, the outlook for Australian agriculture this financial year is for growing production value, and average incomes for broadacre farms are anticipated to increase in 2024-25. This improvement in income supports farmers’ confidence in investing back into their business,” Mr van Doremaele said.

On-farm infrastructure – such as fences, yards and silos – remains the primary focus, although slightly fewer farmers across the country identified this as an area for investment this quarter (58 per cent, was 61 per cent last quarter).

Adopting new technologies was the second highest area of planned investment (31 per cent, down from 36 per cent last quarter), followed by new plant and machinery which was stable quarter-on-quarter at 22 per cent of farmers.

Appetite for rural land purchase remained relatively stable this quarter, with 12 per cent (was 11 per cent) of farmers nationally expressing interest in expanding their farming operation.

A comprehensive monitor of outlook and sentiment in Australian rural industries, the Rabobank Rural Confidence Survey questions an average of 1000 primary producers across a wide range of commodities and geographical areas throughout Australia on a quarterly basis. The most robust study of its type in Australia, the Rabobank Rural Confidence Survey has been conducted since 2000 by an independent research organisation. The next results are scheduled for release in December 2024.

Rabobank Australia & New Zealand Group is a part of the international Rabobank Group, the world’s leading specialist in food and agribusiness banking. Rabobank has more than 125 years’ experience providing customised banking and finance solutions to businesses involved in all aspects of food and agribusiness. Rabobank is structured as a cooperative and operates in 37 countries, servicing the needs of approximately 8.4 million clients worldwide through a network of more than 1000 offices and branches. Rabobank Australia & New Zealand Group is one of Australasia’s leading agricultural lenders and a significant provider of business and corporate banking and financial services to the region’s food and agribusiness sector. The bank has 90 branches throughout Australia and New Zealand.

Media Contacts:

Denise Shaw

Head of Media Relations

Rabobank Australia & New Zealand

Phone: 02 8115 2744 or 0439 603 525

Email: denise.shaw@rabobank.com

Will Banks

Media Relations Manager

Rabobank Australia

Phone: 0418 216 103

Email: will.banks@rabobank.com